Homeownership is often described as the cornerstone of the American Dream—but its influence reaches far beyond real estate. At SFMC Home Lending, we believe buying a home isn’t just about purchasing a place to live—it’s about building a life with deeper roots, financial strength, and long-term possibilities. The ripple effects of owning property are vast, touching every aspect of one’s personal and professional journey.

The Financial Foundation: Building Wealth and Discipline

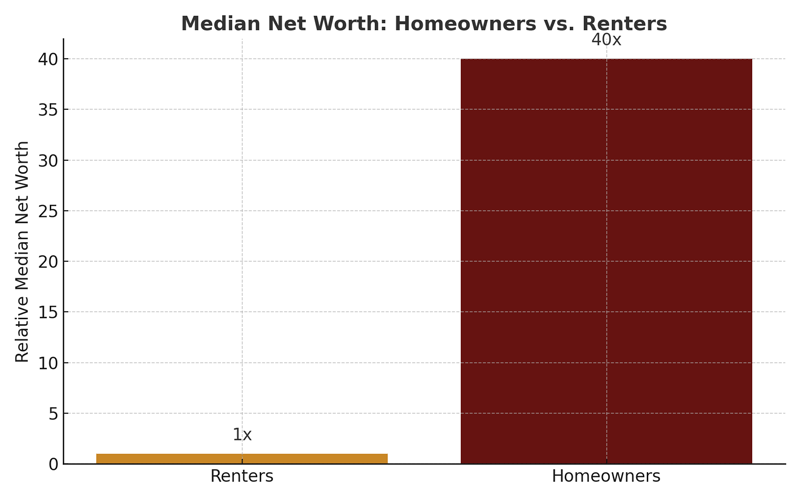

Purchasing a home is one of the most significant financial decisions a person can make. It introduces the concept of forced savings through monthly mortgage payments, builds equity over time, and creates long-term asset growth.

“Homeowners have a median net worth nearly 40 times greater than renters.”

— Federal Reserve Survey of Consumer Finances, 2019

This financial commitment also encourages smarter budgeting, stronger credit discipline, and more intentional spending habits. As homeowners manage property taxes, insurance, and maintenance, they often develop more strategic financial habits that extend into other areas of life.

Career Stability and Confidence

Owning a home can influence career decisions in subtle but meaningful ways. According to a Harvard Joint Center for Housing Studies report, homeowners are more likely to stay in one location, contributing to job tenure and career progression.

- Stability reduces relocation stress, making it easier to commit to long-term roles or promotions.

- Confidence in personal finances often translates to professional confidence, opening doors for career growth.

For those raising a family, homeownership can also provide the predictability needed to evaluate new career opportunities without the additional uncertainty of moving.

Family Planning with Peace of Mind

A home provides more than shelter—it offers a sense of permanence and control over one’s environment. These factors are particularly influential when planning for children or multigenerational living.

- Access to consistent school districts

- Stability in routine and surroundings

- The ability to customize living space to support family needs

Many families cite homeownership as a catalyst for starting or growing their family, prioritizing safety, space, and community ties.

Stronger Community Engagement

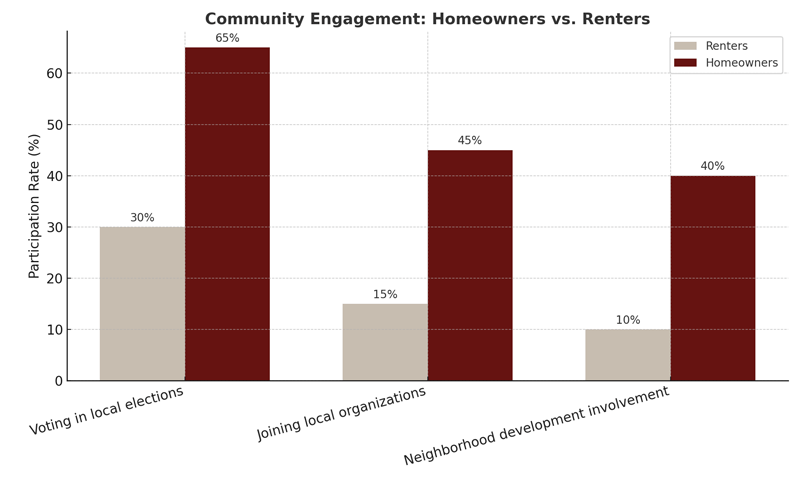

When people own property, they tend to develop a deeper connection to their neighborhoods. Research from the National Association of Realtors (2023) shows that homeowners are significantly more likely to vote, participate in local organizations, and contribute to neighborhood development initiatives.

“Homeowners are more than twice as likely to participate in civic groups than renters.”

— National Association of Realtors, 2023

This engagement often fosters stronger relationships, safer neighborhoods, and more collaborative environments—benefits that extend to everyone in the community.

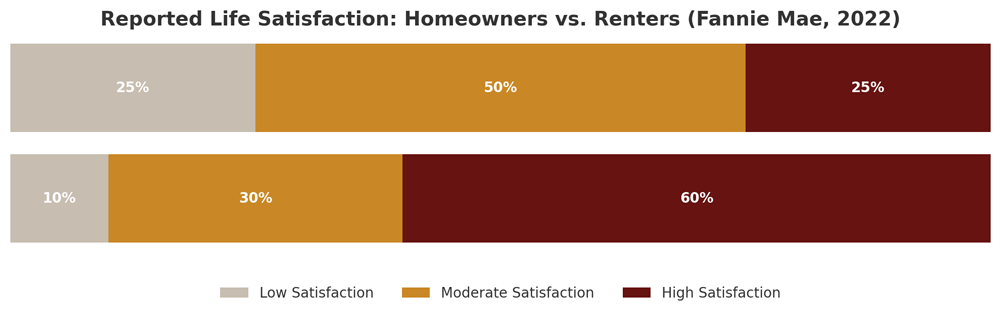

Long-Term Personal and Emotional Wellness

The psychological benefits of homeownership are well documented. A stable living environment can reduce stress, improve mental health, and foster a sense of personal accomplishment.

- Pride in ownership boosts self-esteem

- Consistency in surroundings contributes to emotional stability

- Autonomy over one’s home fosters creativity and satisfaction

A 2022 Fannie Mae study found that homeowners reported significantly higher levels of life satisfaction compared to renters, largely due to these emotional and psychological advantages

Homeownership as a Life Multiplier

At SFMC Home Lending, we’ve seen firsthand how homeownership becomes a multiplier of stability, not just in finances but in every facet of life. From better budgeting to deeper community roots, the ripple effects of owning property are transformative.

If you’re considering buying your first home—or your next—know that you’re investing in far more than square footage. You’re building a life.

References

- Federal Reserve Board. (2019). Survey of Consumer Finances. https://www.federalreserve.gov/econres/scfindex.htm

- Harvard Joint Center for Housing Studies. (2022). The State of the Nation’s Housing 2022. https://www.jchs.harvard.edu/state-nations-housing-2022

- National Association of Realtors. (2023). Social Benefits of Homeownership and Stable Housing. https://www.nar.realtor/reports/social-benefits-of-homeownership-and-stable-housing

- Fannie Mae. (2022). National Housing Survey. https://www.fanniemae.com/research-and-insights/surveys