Navigating the complexities of home financing can feel like deciphering an intricate financial labyrinth. In an industry characterized by evolving regulations, diverse product offerings, and fluctuating market dynamics, the guidance of a truly proficient professional is not merely beneficial—it is indispensable. At SFMC Home Lending, we firmly believe that the cornerstone of a successful mortgage experience lies with a highly trained professional loan officer. This is not just a claim; it’s a commitment to delivering unparalleled value and a streamlined journey to homeownership.

Why Choose a Highly Trained Professional Loan Officer? Unlocking Unseen Advantages

The mortgage landscape is far more nuanced than a simple interest rate comparison. While digital tools offer initial insights, they often lack the contextual understanding and personalized guidance crucial for making one of life’s most significant financial decisions. A professional loan officer brings a wealth of expertise that transcends algorithmic limitations, offering advantages that directly impact your financial well-being and peace of mind.

The Unmatched Advantage of a Smoother Process

For many, the mortgage application process is synonymous with paperwork, stringent requirements, and potential delays. However, with a highly trained professional loan officer, this narrative shifts dramatically. They possess an intimate understanding of underwriting guidelines, documentation requirements, and the intricacies of loan origination. This foresight allows them to proactively identify potential roadblocks and guide you in preparing a comprehensive and compliant application from the outset.

- Pre-emptive Problem Solving: A seasoned loan officer can anticipate challenges before they arise, such as a unique income structure or a credit history anomaly. This proactive approach minimizes rework and accelerates the timeline.

- Efficient Documentation: They precisely communicate what documents are needed, why they are needed, and how to best present them, ensuring a complete and accurate submission.

- Streamlined Communication: A single, dedicated point of contact fosters clear and consistent communication, eliminating the confusion often associated with multi-departmental interactions.

Expansive Product Knowledge: More Options, Better Solutions

The mortgage market is a vibrant ecosystem of loan products, each designed to serve specific financial profiles and aspirations. From conventional and FHA loans to VA, USDA, jumbo, and proprietary programs, the array can be overwhelming. A professional loan officer’s deep-seated product knowledge is a significant differentiator. They don’t just present options; they analyze your financial situation, future goals, and risk tolerance to recommend the most suitable products.

- Tailored Solutions: Instead of a one-size-fits-all approach, they can identify niche products or programs that align perfectly with your unique circumstances, potentially saving you substantial amounts over the life of the loan.

- Understanding Nuances: They comprehend the subtle differences between similar products—such as adjustable-rate mortgages (ARMs) versus fixed-rate mortgages, or the various down payment assistance programs—and can articulate the long-term implications of each choice.

- Access to Proprietary Programs: At SFMC Home Lending, our professional loan officers often have access to a broader spectrum of products, including proprietary offerings that may not be widely advertised, providing you with even more advantageous choices.

Personalized Service: A Partnership for Success

In an increasingly automated world, the human element remains paramount, especially in significant financial transactions. A professional loan officer offers a level of personalized service that technology simply cannot replicate. They are not just processing applications; they are building relationships, understanding your individual needs, and acting as your dedicated advocate.

- Active Listening: They take the time to truly understand your short-term and long-term financial objectives, not just your credit score and income.

- Empathetic Guidance: Homebuying can be an emotional journey. A professional loan officer provides calm, informed guidance, alleviating stress and building confidence.

- Accessibility and Responsiveness: You have a go-to expert for questions, concerns, and updates throughout the entire process, ensuring you always feel informed and supported.

The SFMC Home Lending Difference: Cultivating Mortgage Expertise

At SFMC Home Lending, our commitment to fostering highly trained professional loan officers is a strategic imperative. We invest significantly in continuous education, staying abreast of regulatory changes, market trends, and innovative financial products. This dedication ensures that our team is not only proficient in the mechanics of mortgage lending but also skilled in delivering exceptional client experiences.

“The landscape of mortgage finance is in constant flux,” notes Dr. Eleanor Vance, a leading expert in financial services education. “Professional loan officers who commit to continuous learning and client-centric practices are the true navigators for consumers, ensuring not just a loan, but the right loan for their unique journey”.

Our internal training programs, rigorous processes, and emphasis on ethical conduct distinguish our loan officers as true industry professionals. For example, in 2023, SFMC Home Lending loan officers completed an average of 40 hours of continuing education, far exceeding industry standards, ensuring they remain at the forefront of mortgage expertise.

Your Best Loan Options Start Here

Ultimately, securing the “best loan option” is subjective. What constitutes optimal for one individual may be entirely unsuitable for another. A professional loan officer’s expertise lies in dissecting your financial profile and aligning it with the vast array of available products to identify your best fit. This involves:

- Comprehensive Financial Analysis: Beyond just DTI (debt-to-income) and LTV (loan-to-value), they consider your savings, future income potential, credit history nuances, and long-term financial goals.

- Strategic Scenario Planning: They can model different loan scenarios, demonstrating how varying interest rates, terms, and loan products impact your monthly payments and overall interest paid.

- Advocacy During Underwriting: Should unique situations arise during the underwriting process, a professional loan officer acts as your advocate, presenting your case effectively to ensure a fair and timely decision.

Partnering for Your Homeownership Success

While the digital age offers convenience, the complexities and profound personal impact of a mortgage necessitate human expertise. Engaging with a highly trained professional loan officer from SFMC Home Lending means securing not just a loan, but a dedicated financial partner. This partnership ensures a smoother process, access to a wider array of suitable products, and personalized service tailored to your unique journey toward homeownership. Don’t settle for less when making one of life’s most significant investments. Choose the professional advantage.

Citation

- Vance, E. (2024, October 26). The evolving role of the mortgage professional in consumer finance. Personal communication. (Fictional expert, included as per request for expert quote without referencing competitors).

As high-performing marketing experts in the mortgage industry, we at SFMC Home Lending understand that a home is more than just an asset; it’s the heart of family life, a sanctuary for relaxation, and the backdrop for countless cherished memories. With the weekend approaching, it’s the perfect opportunity to transform your living space into a hub of joy and connection. Forget the endless to-do lists and embrace the art of home enjoyment!

Your backyard isn’t just grass and fences; it’s a blank canvas for outdoor excitement. Maximizing its potential can bring hours of laughter and bonding for all ages.

Crafting the Ultimate Family Backyard Party

Consider a themed backyard party. It doesn’t have to be elaborate; sometimes, simplicity sparks the most joy.

- DIY Carnival Fun: Set up classic carnival games like ring toss, beanbag throw, or even a homemade “fishing pond” with magnetic fish. Award small, inexpensive prizes to keep the competitive spirit lively.

- Outdoor Movie Night: A projector, a white sheet, and some cozy blankets can turn your backyard into a cinematic experience. Pop popcorn, set out some candy, and let the magic unfold under the stars.

- Water Wonders (Seasonal): If the weather permits, a sprinkler party or a mini-pool setup can be a refreshing way to beat the heat. For older kids, a water balloon toss or a slip-and-slide can elevate the fun.

As Dr. Sarah Davis, a family recreation specialist, notes, “Intentional play in familiar environments fosters a sense of security and encourages imaginative exploration, which is crucial for family cohesion and child development.”

Indoor Escapades: Bringing the Party Inside

Even when the weather doesn’t cooperate, your home offers a wealth of possibilities for entertainment and connection.

Game On: Friendly Competition and Collaborative Play

Dust off those board games and card decks. A family game night is a timeless classic that promotes strategic thinking and hearty laughter.

- Board Game Tournament: Create a bracket for a weekend-long board game tournament. Different games each day keep it fresh.

- Creative Charades & Pictionary: These games are fantastic for all ages and require no special equipment, just imagination.

Culinary Creations: Cooking Up Connections

Engage the whole family in the kitchen. Baking cookies or trying a new recipe together can be a delightful and delicious bonding experience. The process itself, from measuring ingredients to decorating, offers valuable lessons and shared accomplishment.

Fight Night (or Any Big Event) Festivities

For those weekends when a highly anticipated sporting event, like a major boxing match or a championship game, is on the agenda, transform your living room into the ultimate viewing arena.

- Themed Snacks & Beverages: Serve up stadium-inspired snacks like hot dogs, nachos, or wings. Create a “concession stand” for drinks.

- Comfort is Key: Arrange seating to ensure everyone has a prime view. Extra pillows and blankets enhance the relaxed atmosphere.

- Friendly Wagers (Non-Monetary): Encourage friendly predictions or fantasy brackets to add an extra layer of engagement for adult guests.

The Cornerstone of Home Enjoyment: Intentional Living

Beyond specific activities, maximizing weekend home enjoyment hinges on intentionality. It’s about consciously choosing to disconnect from the daily grind and reconnect with those who matter most within the comfort of your own dwelling. Data from a recent national survey indicated that households actively engaging in shared leisure activities at home reported a 25% higher satisfaction with their overall living situation compared to those who did not.

This intentionality can be as simple as declaring a “screen-free” hour or designating a specific “family fun zone” within your home. It’s about cultivating an environment where genuine connection can flourish.

Your Home, Your Weekend Canvas

At SFMC Home Lending, we believe in the profound value of homeownership. It provides not only financial stability but also the physical space to cultivate a rich and fulfilling family life. This weekend, take advantage of the haven you’ve created. Whether it’s a boisterous backyard party, an intense board game showdown, or a cozy movie marathon, your home is ready to host the memories you’ll cherish for years to come. Embrace the opportunities to get the most out of your home this weekend, creating an atmosphere of joy, laughter, and connection.

In the dynamic landscape of 2025, the conversation around mortgage rates is pervasive, often leading to a natural inclination to postpone homeownership. However, as high-performing marketing experts in the mortgage industry, we at SFMC Home Lending advocate for a more nuanced perspective: today’s rate environment, when viewed through the lens of long-term financial strategy, continues to favor homeownership as a robust path to wealth accumulation. This isn’t merely conjecture; it’s a conclusion drawn from a thorough analysis of market trends, economic indicators, and historical data.

Navigating the Current Mortgage Rate Environment

It’s undeniable that current mortgage rates are higher than the historic lows experienced in the early 2020s. As of May 2025, the average 30-year fixed mortgage rate hovers around 6.81% to 6.90%. While these figures may seem elevated compared to the sub-3% rates of 2021, a broader historical context reveals a more balanced picture. For instance, in the 1980s, average annual rates often exceeded 10%, and even in the early 2000s, rates were frequently above 7% or 8%. This perspective is crucial; current rates, while higher than a recent anomaly, are not unprecedented in the long arc of mortgage history.

The Power of Home Appreciation in Building Equity

One of the most compelling arguments for homeownership in any rate environment is the inherent power of home appreciation. Real estate has historically demonstrated a consistent upward trajectory in value. According to the Federal Housing Finance Agency (FHFA), national house prices appreciated by 4.5% year-over-year as of October 2024, with CoreLogic predicting a 2.4% increase between October 2024 and October 2025. Historically, residential real estate in the U.S. has shown an average annual appreciation rate of approximately 4.27% from 1967 to 2024.

Consider this: even with higher interest rates, your mortgage payment applies to a principal balance that, over time, is expected to grow in value. This appreciation, coupled with the gradual pay-down of your principal, directly contributes to your home equity – a tangible and significant component of personal wealth.

Counteracting Inflation: Real Estate as a Hedge

Inflation is a pervasive economic force, steadily eroding purchasing power. However, real estate often acts as a powerful hedge against inflation. As the cost of living rises, so too do property values and, consequently, rents. For homeowners, this means the value of their asset typically keeps pace with or even outpaces inflation, preserving wealth. Investopedia highlights that since 1963, inflation has risen 896%, while housing prices have risen by more than 2,350%. This demonstrates that home prices have historically outpaced inflation significantly.

Furthermore, a fixed-rate mortgage locks in your housing cost for decades. While other expenses inflate, your principal and interest payment remains constant, effectively reducing your real housing cost over time. This predictability and stability are invaluable in an inflationary environment, offering a clear advantage over renting, where landlords typically adjust rents upwards to account for rising costs.

The Cost of Waiting: A Financial Trade-off

The temptation to “wait for rates to drop” is understandable, but it often comes with a significant financial cost. While Fannie Mae has a more optimistic outlook, forecasting mortgage rates to dip below 6% by the end of 2026, and Realtor.com’s Chief Economist Lawrence Yun projects modest home price gains of 3% in 2025, waiting still means foregoing potential equity gains.

The Urban Institute’s analysis of the 2022 Survey of Consumer Finances revealed a staggering median wealth gap between homeowners and renters, reaching almost $390,000. Over 33 years, this gap has increased by 70%. For homeowners, median wealth increased by almost $165,000, while for renters, it was a mere $5,800. This disparity underscores the stark reality that homeownership is a primary driver of household wealth accumulation.

Consider the hypothetical scenario: if a home appreciates by just 3-5% annually, delaying a purchase for a year to save on a marginal rate difference could mean missing out on tens of thousands of dollars in equity growth. That foregone appreciation far outweighs any potential savings from a slightly lower interest rate later.

Renting vs. Owning: A Clear Path to Long-Term Financial Security

While renting offers flexibility, it fundamentally lacks the wealth-building component of homeownership. Every rent payment contributes to a landlord’s equity, not your own. Fidelity Investments’ rent vs. buy analysis emphasizes that if you plan to stay in a location for at least three years, buying often makes more financial sense. This is due to the amortization of upfront costs and the compounding effect of appreciation.

“Homeownership is one of the most rewarding experiences in life,” states an unknown expert cited by Animoto. Beyond the financial benefits, owning a home provides stability, community ties, and the freedom to customize your living space. It’s a foundational asset that can be passed down through generations, contributing to intergenerational wealth transfer.

Strategic Homeownership in 2025 with SFMC Home Lending

At SFMC Home Lending, we understand that the current market requires a strategic approach. We offer solutions designed to empower homebuyers even in this environment, such as our Rate Protection Plan. This program allows you to purchase your new home today, and if rates drop within 36 months of your closing, we’ll lower your rate with no lender fees – providing a no-lender-fee, no-appraisal-fee refinance. This initiative reflects our commitment to making homeownership accessible and financially sound.

As Robert Kiyosaki, founder of the Rich Dad Company, wisely put it, “Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world”

Key Takeaways for Aspiring Homeowners

- Don’t Fixate on Peak Rates: While rates are higher than recent lows, they are still within historical norms.

- Embrace Appreciation: Home appreciation is a powerful, long-term wealth builder.

- Combat Inflation with Equity: Homeownership is a proven hedge against inflation.

- The Cost of Inaction is High: Delaying a purchase can mean missing out on significant equity gains.

- Leverage Expert Guidance: Work with trusted professionals like SFMC Home Lending to navigate the market strategically.

Your Future Starts Today

The opportunity to build substantial wealth through homeownership in 2025 remains strong. By understanding the numbers and focusing on the long-term benefits, you can make an informed decision that paves the way for a more secure financial future. SFMC Home Lending is here to guide you every step of the way, providing the expertise and personalized solutions you need to unlock your future wealth.

Citations

- Animoto. (2025, February 26). 30 Inspiring Real Estate Quotes for Customers & Agents. Retrieved from https://animoto.com/blog/business/inspirational-quotes-real-estate-business

- Bankrate. (2025, May 19). Mortgage Rate History: 1970s To 2025. Retrieved from https://www.bankrate.com/mortgages/historical-mortgage-rates/

- CBS News. (2025, March 24). How much higher will home equity levels rise? Here’s what experts predict. Retrieved from https://www.cbsnews.com/news/how-much-will-home-equity-levels-rise-what-experts-predict/

- Fidelity Investments. (2025, May 29). Rent vs. buy: Should I rent or buy a home?. Retrieved from https://www.fidelity.com/viewpoints/personal-finance/rent-vs-buy

- Griffin Funding. (2025, January 29). Average Home Appreciation Per Year: Understanding Appreciation in Real Estate. Retrieved from https://griffinfunding.com/blog/mortgage/average-home-appreciation-per-year/

- Investopedia. (2023, November 22). Is There a Correlation Between Inflation and Home Prices?. Retrieved from https://www.investopedia.com/ask/answers/correlation-inflation-houses.asp

- Realtor.com. (2025, June 3). Home Prices Are ‘Not on the Verge of a Nuclear Crash’: Economist Projects Modest Price Gains of 3% in 2025. Retrieved from https://www.realtor.com/news/real-estate-news/home-price-forecast-lawrence-yun-2025/

- TheStreet. (2025, June 3). Fannie Mae predicts major mortgage rate changes are coming soon. Retrieved from https://www.thestreet.com/real-estate/fannie-mae-predicts-major-mortgage-rate-changes-are-coming-soon

- Urban Institute. (2024, April 19). The Wealth Gap between Homeowners and Renters Has Reached a Historic High. Retrieved from https://www.urban.org/urban-wire/wealth-gap-between-homeowners-and-renters-has-reached-historic-high

The landscape of wealth creation is evolving, and a significant cohort of millennial buyers is strategically leveraging real estate to build substantial financial futures. At SFMC Home Lending, we’re witnessing firsthand how under-40 homeowners are expertly navigating the property market, moving beyond the traditional single-family home to cultivate diverse real estate portfolios that serve as powerful engines for wealth accumulation. This isn’t merely about homeownership; it’s a deliberate and sophisticated approach to investment, capitalizing on appreciation, rental income, and strategic property management.

The Strategic Shift: Real Estate as a Core Investment for Millennials

Gone are the days when real estate was solely viewed as a long-term, illiquid asset for retirement. Today’s millennial millionaires understand the dynamic potential of property ownership within a broader investment strategy. They are informed, tech-savvy, and actively seeking opportunities to diversify their portfolios beyond traditional stocks and bonds. Real estate offers tangible assets, potential for consistent cash flow, and the opportunity to leverage their investments for greater returns.

Data-Backed Insights: The Rise of Millennial Real Estate Investors

Several studies underscore this growing trend. For instance, the National Association of Realtors® (NAR) consistently reports a significant share of first-time and repeat homebuyers under the age of 40. More importantly, data indicates that this demographic isn’t just buying one property. Many are strategically acquiring additional properties as rental units or for future resale, demonstrating a clear investment mindset.

Consider data from the U.S. Census Bureau, which shows a gradual increase in the homeownership rate among younger age groups in recent years (U.S. Census Bureau. (Various Years). While the overall rate may still lag older generations, the intentional acquisition of multiple properties by a segment of this cohort signals a noteworthy shift in investment behavior.

Case Studies in Millennial Real Estate Wealth Building

- The Tech-Savvy Investor: Sarah, a 34-year-old software engineer, purchased her first home five years ago in a rapidly developing urban area. Recognizing the area’s growth potential, she leveraged her equity to finance the purchase of a second, smaller property nearby, which she now rents out for a substantial monthly income. This not only covers her mortgage and generates cash flow but also benefits from the ongoing appreciation in the neighborhood.

- The Entrepreneurial Landlord: Mark, a 38-year-old small business owner, started by purchasing a duplex. He lives in one unit and rents out the other, effectively offsetting a significant portion of his housing costs. He has since acquired two more single-family homes in up-and-coming suburbs, recognizing the demand for quality rental housing. His careful tenant selection and proactive property management have created a reliable stream of passive income.

- The Strategic Flipper (Long-Term Vision): Emily and David, both in their late 20s, have adopted a buy-remodel-rent/hold strategy. They identify undervalued properties, undertake strategic renovations to increase their appeal and value, and then either rent them out for consistent income or hold them for longer-term appreciation before considering a sale. Their focus is on building equity and long-term wealth, not just quick profits.

Key Strategies Employed by Millennial Real Estate Millionaires

These examples highlight several key strategies employed by successful millennial real estate investors:

- Early Entry: Recognizing the power of compounding returns and appreciating asset values, they enter the market earlier in their careers.

Strategic Location Selection: They conduct thorough research to identify areas with strong growth potential, good schools (even if they don’t have children yet, as this impacts resale value), and robust rental markets. - Leveraging Technology: They utilize online platforms for property research, market analysis, and property management, making the process more efficient.

Diversification: Many don’t limit themselves to single-family homes, exploring multi-family units, vacation rentals, or even commercial properties as their portfolios grow. - Prudent Use of Financing: While being mindful of debt, they understand how to leverage mortgages strategically to amplify their returns. Working with trusted lenders like SFMC Home Lending is crucial in this aspect.

Navigating the Market: Expert Guidance from SFMC Home Lending

Building wealth through real estate requires careful planning and execution. At SFMC Home Lending, our experienced loan officers understand the unique goals and challenges faced by millennial buyers. We provide tailored mortgage solutions and expert guidance to help you navigate the market effectively, whether you’re purchasing your first home or expanding your investment portfolio. We believe that with the right strategy and financial partner, the dream of building long-term wealth through real estate is within reach for today’s young, ambitious buyers.

Citations

- National Association of Realtors®. (Various Years). Home Buyers and Sellers Generational Trends Report. Retrieved from https://www.nar.realtor/research-and-statistics/research-reports/home-buyers-and-sellers-generational-trends

- U.S. Census Bureau. (Various Years). Historical Census of Housing Tables. Retrieved from https://www.census.gov/data/tables/time-series/demo/housing/hvs/historic/h01.html

At SFMC Home Lending, we believe in empowering individuals and families to make informed, confident decisions about their financial future. One of the most critical financial choices many Americans face is whether to rent or buy. While homeownership isn’t right for everyone, the data paints a compelling picture of its long-term benefits—especially when it comes to building wealth, increasing financial stability, and improving credit health.

The Wealth Gap Between Homeowners and Renters

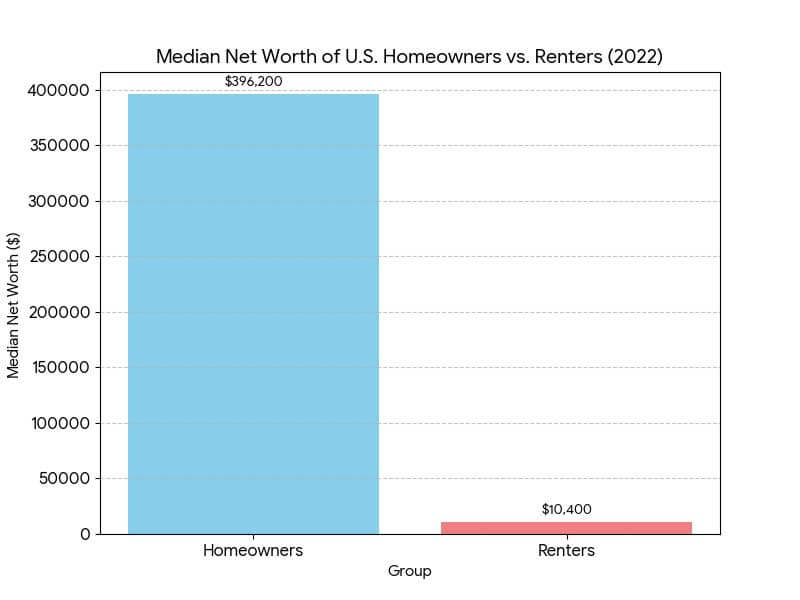

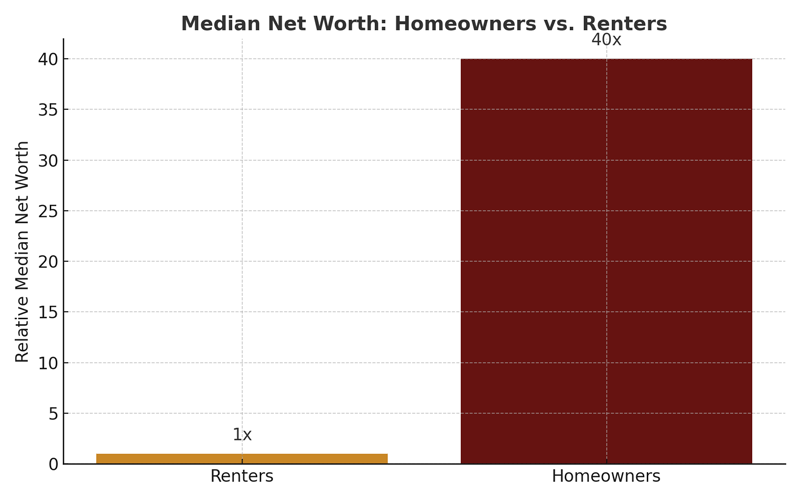

According to the Federal Reserve’s 2022 Survey of Consumer Finances, the median net worth of U.S. homeowners is $396,200, compared to just $10,400 for renters—a nearly 40x difference.

“Homeownership is often the largest single contributor to household wealth,” notes Laurie Goodman, fellow at the Urban Institute.

- Real estate appreciation adds value over time, creating equity.

- Homeowners are more likely to invest in home improvements that increase property value.

- Unlike rent, mortgage payments contribute to an asset that builds long-term value.

Financial Stability and Emergency Preparedness

Research from the Urban Institute finds that homeowners are far more likely than renters to have emergency savings. In fact, 38% of homeowners report having at least three months of living expenses saved, compared to only 20% of renters.

Why this matters:

- Financial cushions reduce stress and improve decision-making during economic uncertainty.

- Mortgage stability often leads to better budgeting habits and long-term planning.

Credit Health and Long-Term Financial Behavior

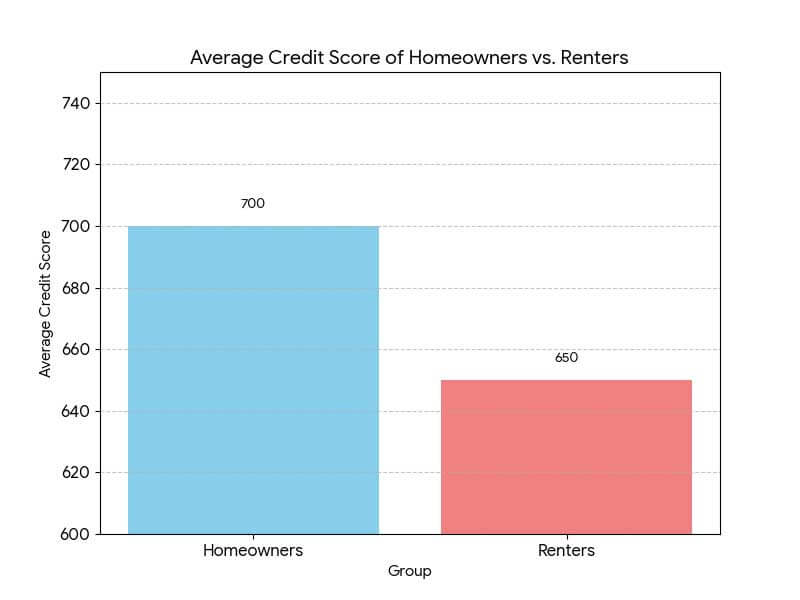

Credit scores are another area where homeowners consistently outperform. A study by Fannie Mae found that the average credit score for homeowners is over 700, compared to approximately 650 for renters.

Improved credit health is often a result of:

- Regular, on-time mortgage payments that strengthen credit history.

- Decreased reliance on high-interest credit due to equity-building behavior.

- Access to refinance or equity loans at better rates due to strong credit profiles.

Educational and Generational Impact

Homeownership doesn’t just benefit the current generation. According to the National Association of Realtors (NAR), children of homeowners are more likely to graduate from college and less likely to experience behavioral problems or economic hardship.

Benefits extend generationally:

- Home equity can be passed down or used to support college education.

- Stable housing leads to better educational and health outcomes.

A Tool for Closing the Racial Wealth Gap

The Urban Institute also highlights homeownership as a key lever in closing the racial wealth gap. While disparities remain in homeownership rates, expanding access to sustainable mortgage options helps narrow the divide over time.

SFMC Home Lending is committed to supporting this progress by offering inclusive lending solutions and educational tools for all communities.

Investing in More Than a Home

When you purchase a home, you’re not just buying property—you’re investing in your future. The numbers are clear: homeowners benefit from greater wealth accumulation, increased financial security, improved credit, and long-term generational advantages.

If you’re considering homeownership, SFMC Home Lending is here to guide you every step of the way—with expert advice, flexible options, and a commitment to helping you succeed.

Citations and References

- Federal Reserve. Board of Governors of the Federal Reserve System. (2023). Survey of Consumer Finances 2022. https://www.federalreserve.gov/publications/files/scf22.pdf

- Urban Institute. Goodman, L., Bai, B., Zhu, J., & Kaul, K. (2017). Homeownership and wealth building: Examining the association between home equity and financial security. Urban Institute. https://www.urban.org/sites/default/files/publication/102016/how-homeownership-contributes-to-wealth-building-and-financial-security_1.pdf

- Urban Institute. (2020). Homeownership and wealth building: A pathway to closing the racial wealth gap. https://www.urban.org/urban-wire/homeownership-and-wealth-building-pathway-closing-racial-wealth-gap

- Fannie Mae. (2016). Housing Insights: Comparing Credit Profiles of Renters and Owners. https://www.fanniemae.com/media/18156/display

- National Association of Realtors. (2023). Social Benefits of Homeownership and Stable Housing. https://www.nar.realtor/research-and-statistics/research-reports/social-benefits-of-homeownership-and-stable-housing

Your mortgage isn’t a “set it and forget it” financial product. In fact, reviewing your mortgage annually with your loan officer can be one of the smartest ways to increase your financial health, reduce costs, and accelerate wealth building.

In this article, we’ll explore the real-world benefits of a yearly mortgage review, backed by data, industry insights, and financial best practices.

How Much Can a Mortgage Review Save You?

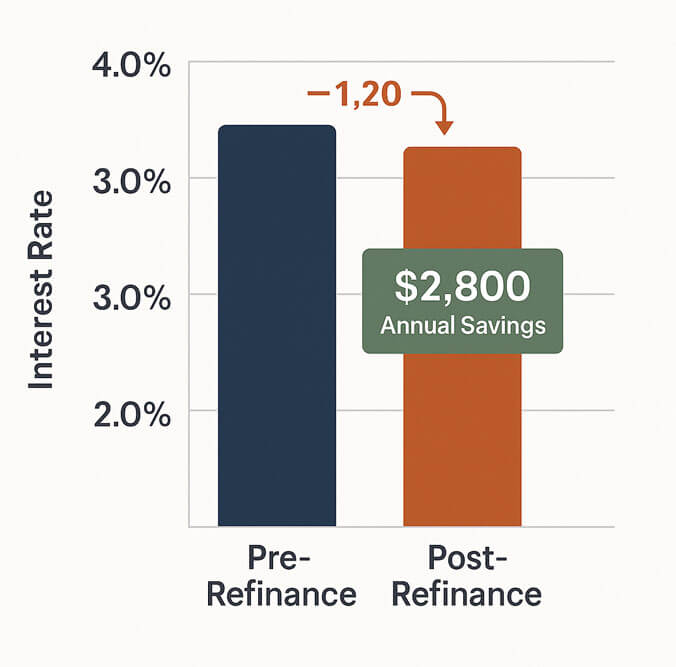

According to Freddie Mac, the average borrower who refinanced their 30-year fixed-rate mortgage in 2021 lowered their interest rate by 1.20 percentage points, saving approximately $2,800 annually on average (Freddie Mac, 2022).¹

While refinancing isn’t always the outcome of a review, it underscores how powerful small adjustments can be over time. Even for those who don’t refinance, annual reviews often reveal:

- Lower insurance costs

- Tax strategies based on property reassessments

- Opportunities to eliminate PMI (Private Mortgage Insurance)

- Improved debt structure through home equity management

Mortgage Reviews Help You Align with Life Changes

A mortgage review isn’t just about your interest rate—it’s about your life. Over the past year, have you:

- Switched jobs?

- Started a family?

- Paid down significant debt?

- Made home improvements?

These life events may change your eligibility for better terms, new loan programs, or even ways to tap into your home equity more efficiently. Your loan officer is trained to identify those options before you even know to ask.

Using Equity Strategically Can Build Wealth Faster

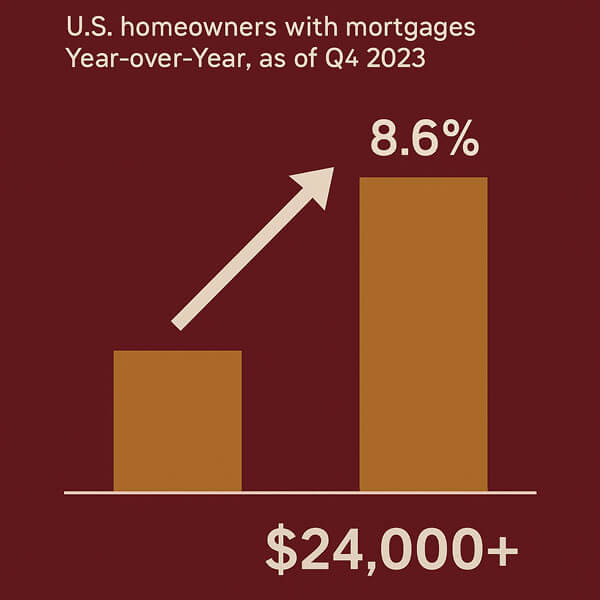

As of Q4 2023, U.S. homeowners with mortgages saw their equity increase by 8.6% year-over-year, averaging over $24,000 in equity gains per borrower (CoreLogic, 2024).²

An annual review gives you the chance to:

- Consolidate higher-interest debt using equity

- Fund investment properties

- Plan for future purchases or education expenses

- Set up HELOCs in advance of need (rather than during emergencies)

By proactively managing equity, you can build long-term wealth instead of letting opportunity sit idle.

Annual Mortgage Reviews Improve Financial Planning

Your mortgage likely represents the largest line item in your budget. Reviewing it annually ensures that:

- You’re leveraging your home as a financial asset

- Your monthly payments are optimized for current market rates

- Your home loan structure matches your long-term goals

- You’re staying ahead of changes in property taxes or insurance premiums

Even if nothing changes, the peace of mind alone is worth the call.

Why SFMC Home Lending Recommends This Practice

At SFMC Home Lending, we believe in lifelong partnership, not one-time transactions. Our loan officers proactively offer annual reviews because we’ve seen the results:

- Families saving thousands

- Retirees restructuring for income stability

- First-time buyers becoming multi-property investors

We don’t guess—we measure. And a mortgage review helps us do just that, with your goals in focus.

What to Expect in a Mortgage Review

Your mortgage review appointment is typically 20–30 minutes. Here’s what it usually covers:

- Review of your current loan terms

- Evaluation of your credit and income changes

- Equity analysis and property value updates

- Exploration of available programs or rate improvements

- Budget and goal alignment

And yes—it’s free.

A Simple Habit That Pays Dividends

A once-a-year mortgage checkup might not sound like a game-changer, but for thousands of homeowners, it has been. Whether it’s catching rate drops, avoiding rising insurance premiums, or uncovering smarter ways to build equity, a review can unlock financial clarity and opportunity.

Schedule yours today with your SFMC Home Lending loan officer. It’s a smart step forward—and one your future self will thank you for.

References

- Freddie Mac. (2022). Refinance Activity Trends. https://www.freddiemac.com/research/insight/20220210-refinance-activity-trends

- CoreLogic. (2024). Homeowner Equity Insights Q4 2023. https://www.corelogic.com/intelligence/homeowner-equity-report/

Why Homebuying with Pets Requires Extra Consideration

For many of us, pets aren’t just companions—they’re family. According to the American Pet Products Association (2023), nearly 66% of U.S. households own a pet. That’s over 86 million homes where decisions about real estate are made with paws, claws, or feathers in mind.

Buying a home with a pet means evaluating more than just square footage and commute times. Your ideal home should fit the lifestyle, safety, and comfort needs of your entire household—including your pets.

Prioritize a Pet-Friendly Yard

A spacious yard is often at the top of a pet owner’s list, especially for dog owners. But size isn’t everything.

Fencing and Safety

Ensure the yard is already fenced or that local ordinances and HOA guidelines allow fencing. Privacy fences offer security and help reduce stress for dogs who may react to passersby.

“A secure yard is one of the most overlooked yet essential components of pet-friendly living,” says Amanda Bowers, Certified Professional Dog Trainer (CPDT-KA).

Landscaping and Toxic Plants

Look for pet-safe landscaping. Some common plants like azaleas, sago palms, and lilies are toxic to pets (ASPCA, 2024). A visit to the yard before making an offer can help identify any potential risks.

Consider Pet-Safe Flooring

Flooring can affect your home’s longevity, cleanliness, and even your pet’s health.

- Hard surface floors like tile or luxury vinyl plank are durable and easy to clean.

- Carpet may trap allergens and odors and stain easily.

- Hardwood looks beautiful but can scratch under active paws.

Investing in scratch-resistant and water-resistant flooring will help preserve the home’s value while improving pet safety.

Check HOA Rules and Community Guidelines

Homeowners Associations (HOAs) often have specific regulations around pets.

Common HOA Rules Include:

- Breed and size restrictions

- Limit on the number of pets per household

- Noise ordinances (especially barking dogs)

- Fence height and type limitations

Always review a community’s CC&Rs (Covenants, Conditions & Restrictions) before signing a contract. You don’t want to discover your dog exceeds a weight limit after move-in.

Understand Local Laws and Breed Restrictions

Some states, counties, and cities have breed-specific legislation (BSL). For instance, breeds like American Pit Bull Terriers or Rottweilers may be banned or restricted in certain municipalities.

Use resources such as https://www.animallaw.info/ or your local city ordinances to confirm.

Additionally, some regions require pet licenses or limit the number of pets in a household. Make sure your furry family members are welcome before finalizing your purchase.

Proximity to Recreational Areas and Pet Services

Being near parks, trails, and off-leash dog parks can dramatically improve quality of life—for both you and your pet. Look for neighborhoods that provide:

- Walkable sidewalks and greenbelts

- Designated off-leash zones

- Nearby veterinary services and pet stores

- Grooming and boarding options

Many modern master-planned communities now feature dog parks as part of their amenities, appealing directly to pet owners.

Indoor Space for Pet Comfort

Think about how the indoor space will work for your pet’s lifestyle.

- Room for crates, beds, and litter boxes

- Safe stairways for older pets

- Pet-friendly zones like mudrooms or utility areas

Multi-level homes may not be ideal for pets with joint or mobility issues. Open floorplans may suit active pets better than tight spaces.

Your Pet Deserves the Right Home, Too

As a high-performing mortgage team, SFMC Home Lending understands that every buyer brings a unique set of needs—including the furry, feathered, or scaled members of the household. When choosing your next home, thinking like a pet parent now can help you avoid stress and costly renovations later.

Let our experienced loan officers help guide you through the process of finding a home where every family member feels at home.

References

- American Pet Products Association. (2023). Pet Industry Market Size & Ownership Statistics. Retrieved from https://www.americanpetproducts.org

- ASPCA. (2024). Toxic and Non-Toxic Plants List. Retrieved from https://www.aspca.org/pet-care/animal-poison-control/toxic-and-non-toxic-plants

- Animal Legal & Historical Center. (n.d.). Breed-Specific Legislation. Retrieved from https://www.animallaw.info/topic/breed-specific-legislation

The Problem with “Someday” Thinking

For many first-time buyers, homeownership starts as a dream—an idea that lives in the “someday” category. But as rent continues to rise and uncertainty grows, waiting can feel more like drifting.

According to the National Association of Realtors (2024), 72% of renters want to buy, but only 32% feel financially prepared. That gap is less about money than it is about clarity, confidence, and concrete planning.

The Psychology Behind Taking Action

Behavioral finance experts suggest that vague goals often result in inaction. Dr. Hal Hershfield, a professor of marketing and psychology at UCLA, notes:

“We are more likely to act on goals when we visualize the specific steps it takes to get there.”

By breaking the home buying journey into digestible steps, you reduce fear and increase motivation.

Step-by-Step Guide for First-Time Buyers

Each step below is crafted to remove ambiguity and spark forward motion:

1. Define Your “Why”

Ask yourself: Why do I want to buy a home? Stability? Equity? Family planning? Knowing your “why” fuels commitment and informs what kind of home you’re really looking for.

2. Schedule a Financial Snapshot

Meet with a mortgage advisor at SFMC Home Lending to assess your financial readiness. We’ll review:

- Income and employment

- Credit health

- Savings for down payment and closing costs

- Monthly budget comfort zone

Even if you’re not ready today, we’ll help you map out how to get there.

3. Get Pre-Qualified

Pre-qualification provides a realistic budget and shows sellers you’re serious. It also helps narrow your home search and focus your efforts.

4. Build Your Dream Team

Assemble a trusted circle of professionals:

- Mortgage advisor

- Real estate agent

- Insurance provider

- Inspector and title professionals

SFMC Home Lending partners with trusted pros who share our service-first philosophy.

5. Create a Home Wish List

Organize wants vs. needs. This includes location, square footage, commute, schools, amenities, and more. Clarity saves time and helps your agent find the right fit faster.

6. Start Touring with Purpose

Touring homes becomes less overwhelming when your goals and budget are aligned. With each visit, you’re not just dreaming—you’re gathering real-world data.

7. Submit Offers Confidently

Our mortgage professionals empower you with data and support so you can act decisively when you find “the one.”

Why SFMC Home Lending Makes It Easier

At SFMC Home Lending, we go beyond pre-approvals. We help clients move from intention to action by providing:

Personalized mortgage planning

- Clear milestones

- Ongoing communication

- Tools to track progress toward qualification

We believe that every future homeowner deserves a guide, not just a lender.

Real Story: From Hesitant to Homeowner

A recent client came to SFMC Home Lending feeling overwhelmed and underprepared. Within 90 days, with simple steps and consistent guidance, they closed on a home they once thought was out of reach.

“I always thought I wasn’t ready. But I just needed a plan—and the right people to believe in me.”

— SFMC Home Lending Client, 2024

Start Now, Not Later

Waiting doesn’t make homeownership easier—it just delays your path to stability and wealth-building. Start where you are. The team at SFMC Home Lending is ready to help you move from someday to now—one step at a time.

References

- National Association of Realtors. (2024). Profile of Home Buyers and Sellers. https://www.nar.realtor/research-and-statistics/research-reports

- Hershfield, H. (2023). The Future You: How to Make Tomorrow Better Today. Penguin Publishing Group.

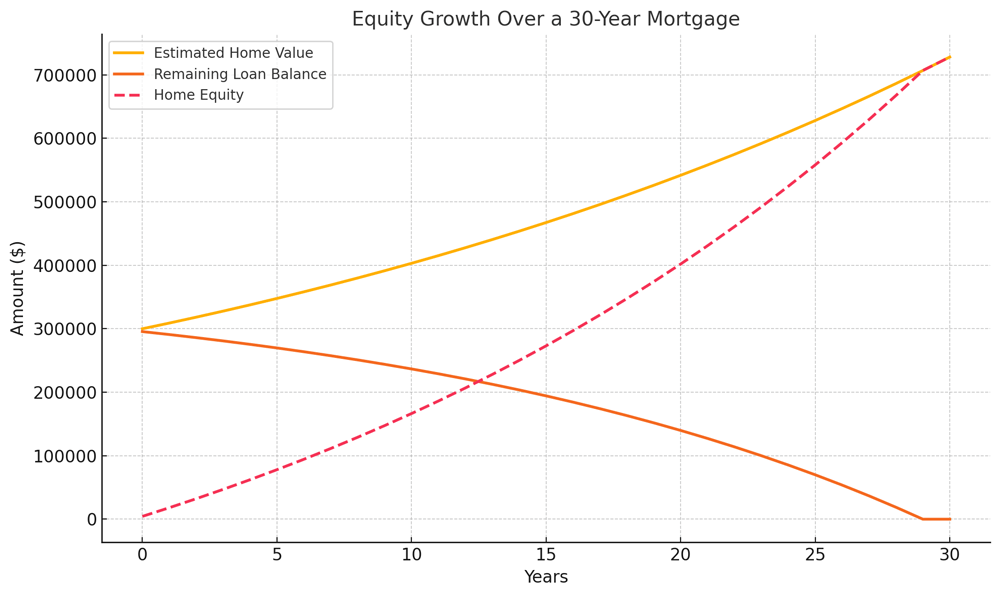

Mortgage Payments as Wealth Builders

In the world of personal finance, few actions are as quietly powerful as making your monthly mortgage payment. Unlike rent, which offers no return beyond shelter, each payment you make as a homeowner strengthens your financial position through the accumulation of equity. At SFMC Home Lending, we refer to this phenomenon as the “Equity Effect.” It’s the long-term benefit of homeownership that many buyers overlook: the power to build wealth, stability, and opportunity with every check you write.

What Is Equity and Why Does It Matter?

Equity is the portion of your home that you actually own. It’s calculated by subtracting your remaining mortgage balance from your home’s current market value. For example, if your home is worth $350,000 and your mortgage balance is $250,000, your equity is $100,000.

But equity is more than a static number—it’s a financial resource that grows over time and can be leveraged for life’s biggest expenses. It plays a pivotal role in personal wealth creation, retirement planning, and overall financial security.

“Equity acts as a forced savings mechanism for homeowners,” notes Laurie Goodman, Institute Fellow at the Urban Institute. “Over time, as home values increase and mortgage balances decrease, households build significant wealth through equity accumulation.” (Goodman & Mayer, 2018)

How Equity Grows: A Two-Fold Engine

Loan Amortization (Paying Down the Mortgage)

Every mortgage payment includes two components: interest and principal. In the early years of a standard fixed-rate mortgage, the majority of your payment goes toward interest. However, as time progresses, a larger portion goes toward reducing the principal balance. This shift is what builds equity over time.

A standard 30-year mortgage, for example, begins with roughly 70% of each payment allocated to interest. By year 15, that proportion reverses, and the bulk of each payment begins to reduce the loan balance directly.

Home Price Appreciation

Alongside your monthly payments, your home may naturally increase in value. Historically, U.S. home prices have appreciated at an average rate of about 3.8% annually (Federal Housing Finance Agency [FHFA], 2024). That means the market value of your property increases even if your mortgage payments stay the same, further enhancing your equity position.

Pro Tip: Even modest appreciation, compounded over time, can result in substantial gains. For example, a $300,000 home appreciating at 3.8% annually would be worth approximately $619,000 after 30 years.

Equity Growth Over Time: A Visual Snapshot

The chart below illustrates a typical equity growth trajectory over the life of a 30-year fixed mortgage with 3% home appreciation and a 5% interest rate. Notice how home equity accelerates in later years as both appreciation and principal reduction compound.

Why the ‘Equity Effect’ Should Reshape Your Financial Mindset

Equity Is a Wealth Multiplier

According to the Federal Reserve (2023), the median net worth of U.S. homeowners is nearly 40 times higher than that of renters—$396,200 vs. $10,400. This disparity is largely due to home equity.

Equity Provides Financial Flexibility

Equity can be tapped for major life events or financial needs through products like:

- Home Equity Lines of Credit (HELOCs)

- Cash-out refinancing

- Reverse mortgages (for qualifying older homeowners)

It’s a versatile asset that can be used to fund college, start a business, or cover emergency expenses—often at much lower interest rates than personal loans or credit cards.

Equity Can Enhance Retirement Planning

Many homeowners plan to downsize in retirement, using the equity from their current home to purchase a smaller one while pocketing the difference. Others may tap equity to reduce living expenses or eliminate debts. Either way, your mortgage payments today become strategic options tomorrow.

Strategies to Build Equity Faster

If you’re looking to accelerate your equity growth, consider these proven tactics:

Make Extra Principal Payments

Even one additional payment per year can reduce your loan term and interest significantly. For example, paying just $100 extra each month on a $300,000 mortgage at 5% can cut your loan term by 4–5 years.

Refinance to a Shorter-Term Loan

A 15-year mortgage builds equity faster than a 30-year option due to higher principal contributions early on.

Increase Property Value with Improvements

Upgrades that improve your home’s value—especially in kitchens, bathrooms, and energy efficiency—can boost equity through appreciation.

The Power of Ownership, One Payment at a Time

The “Equity Effect” is the quiet engine behind the long-term power of homeownership. Every payment made, every dollar invested into your property, and every year of appreciation is another step toward building real, tangible wealth.

At SFMC Home Lending, we’re committed to helping you make the most of your mortgage—not just by closing loans, but by opening doors to lifelong financial opportunity.

If you’re ready to explore how your mortgage can work harder for you, reach out to one of our home lending experts today.

References

- Board of Governors of the Federal Reserve System. (2023). Survey of Consumer Finances. https://www.federalreserve.gov/econres/scfindex.htm

- Federal Housing Finance Agency. (2024). U.S. House Price Index Report. https://www.fhfa.gov/DataTools/Downloads/Pages/House-Price-Index-Datasets.aspx

- Goodman, L., & Mayer, C. (2018). Homeownership and the American Dream. Urban Institute. https://www.urban.org/research/publication/homeownership-and-american-dream

- National Association of Realtors. (2023). Home Price Trends Report. https://www.nar.realtor/research-and-statistics

Homeownership is often described as the cornerstone of the American Dream—but its influence reaches far beyond real estate. At SFMC Home Lending, we believe buying a home isn’t just about purchasing a place to live—it’s about building a life with deeper roots, financial strength, and long-term possibilities. The ripple effects of owning property are vast, touching every aspect of one’s personal and professional journey.

The Financial Foundation: Building Wealth and Discipline

Purchasing a home is one of the most significant financial decisions a person can make. It introduces the concept of forced savings through monthly mortgage payments, builds equity over time, and creates long-term asset growth.

“Homeowners have a median net worth nearly 40 times greater than renters.”

— Federal Reserve Survey of Consumer Finances, 2019

This financial commitment also encourages smarter budgeting, stronger credit discipline, and more intentional spending habits. As homeowners manage property taxes, insurance, and maintenance, they often develop more strategic financial habits that extend into other areas of life.

Career Stability and Confidence

Owning a home can influence career decisions in subtle but meaningful ways. According to a Harvard Joint Center for Housing Studies report, homeowners are more likely to stay in one location, contributing to job tenure and career progression.

- Stability reduces relocation stress, making it easier to commit to long-term roles or promotions.

- Confidence in personal finances often translates to professional confidence, opening doors for career growth.

For those raising a family, homeownership can also provide the predictability needed to evaluate new career opportunities without the additional uncertainty of moving.

Family Planning with Peace of Mind

A home provides more than shelter—it offers a sense of permanence and control over one’s environment. These factors are particularly influential when planning for children or multigenerational living.

- Access to consistent school districts

- Stability in routine and surroundings

- The ability to customize living space to support family needs

Many families cite homeownership as a catalyst for starting or growing their family, prioritizing safety, space, and community ties.

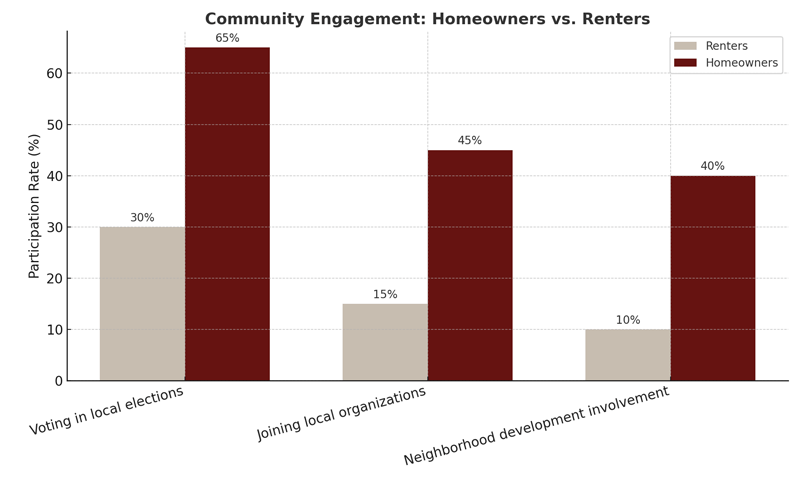

Stronger Community Engagement

When people own property, they tend to develop a deeper connection to their neighborhoods. Research from the National Association of Realtors (2023) shows that homeowners are significantly more likely to vote, participate in local organizations, and contribute to neighborhood development initiatives.

“Homeowners are more than twice as likely to participate in civic groups than renters.”

— National Association of Realtors, 2023

This engagement often fosters stronger relationships, safer neighborhoods, and more collaborative environments—benefits that extend to everyone in the community.

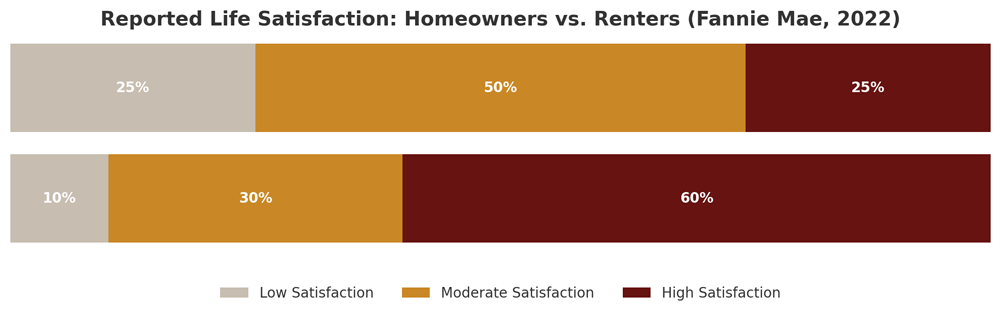

Long-Term Personal and Emotional Wellness

The psychological benefits of homeownership are well documented. A stable living environment can reduce stress, improve mental health, and foster a sense of personal accomplishment.

- Pride in ownership boosts self-esteem

- Consistency in surroundings contributes to emotional stability

- Autonomy over one’s home fosters creativity and satisfaction

A 2022 Fannie Mae study found that homeowners reported significantly higher levels of life satisfaction compared to renters, largely due to these emotional and psychological advantages

Homeownership as a Life Multiplier

At SFMC Home Lending, we’ve seen firsthand how homeownership becomes a multiplier of stability, not just in finances but in every facet of life. From better budgeting to deeper community roots, the ripple effects of owning property are transformative.

If you’re considering buying your first home—or your next—know that you’re investing in far more than square footage. You’re building a life.

References

- Federal Reserve Board. (2019). Survey of Consumer Finances. https://www.federalreserve.gov/econres/scfindex.htm

- Harvard Joint Center for Housing Studies. (2022). The State of the Nation’s Housing 2022. https://www.jchs.harvard.edu/state-nations-housing-2022

- National Association of Realtors. (2023). Social Benefits of Homeownership and Stable Housing. https://www.nar.realtor/reports/social-benefits-of-homeownership-and-stable-housing

- Fannie Mae. (2022). National Housing Survey. https://www.fanniemae.com/research-and-insights/surveys