Mortgage Payments as Wealth Builders

In the world of personal finance, few actions are as quietly powerful as making your monthly mortgage payment. Unlike rent, which offers no return beyond shelter, each payment you make as a homeowner strengthens your financial position through the accumulation of equity. At SFMC Home Lending, we refer to this phenomenon as the “Equity Effect.” It’s the long-term benefit of homeownership that many buyers overlook: the power to build wealth, stability, and opportunity with every check you write.

What Is Equity and Why Does It Matter?

Equity is the portion of your home that you actually own. It’s calculated by subtracting your remaining mortgage balance from your home’s current market value. For example, if your home is worth $350,000 and your mortgage balance is $250,000, your equity is $100,000.

But equity is more than a static number—it’s a financial resource that grows over time and can be leveraged for life’s biggest expenses. It plays a pivotal role in personal wealth creation, retirement planning, and overall financial security.

“Equity acts as a forced savings mechanism for homeowners,” notes Laurie Goodman, Institute Fellow at the Urban Institute. “Over time, as home values increase and mortgage balances decrease, households build significant wealth through equity accumulation.” (Goodman & Mayer, 2018)

How Equity Grows: A Two-Fold Engine

Loan Amortization (Paying Down the Mortgage)

Every mortgage payment includes two components: interest and principal. In the early years of a standard fixed-rate mortgage, the majority of your payment goes toward interest. However, as time progresses, a larger portion goes toward reducing the principal balance. This shift is what builds equity over time.

A standard 30-year mortgage, for example, begins with roughly 70% of each payment allocated to interest. By year 15, that proportion reverses, and the bulk of each payment begins to reduce the loan balance directly.

Home Price Appreciation

Alongside your monthly payments, your home may naturally increase in value. Historically, U.S. home prices have appreciated at an average rate of about 3.8% annually (Federal Housing Finance Agency [FHFA], 2024). That means the market value of your property increases even if your mortgage payments stay the same, further enhancing your equity position.

Pro Tip: Even modest appreciation, compounded over time, can result in substantial gains. For example, a $300,000 home appreciating at 3.8% annually would be worth approximately $619,000 after 30 years.

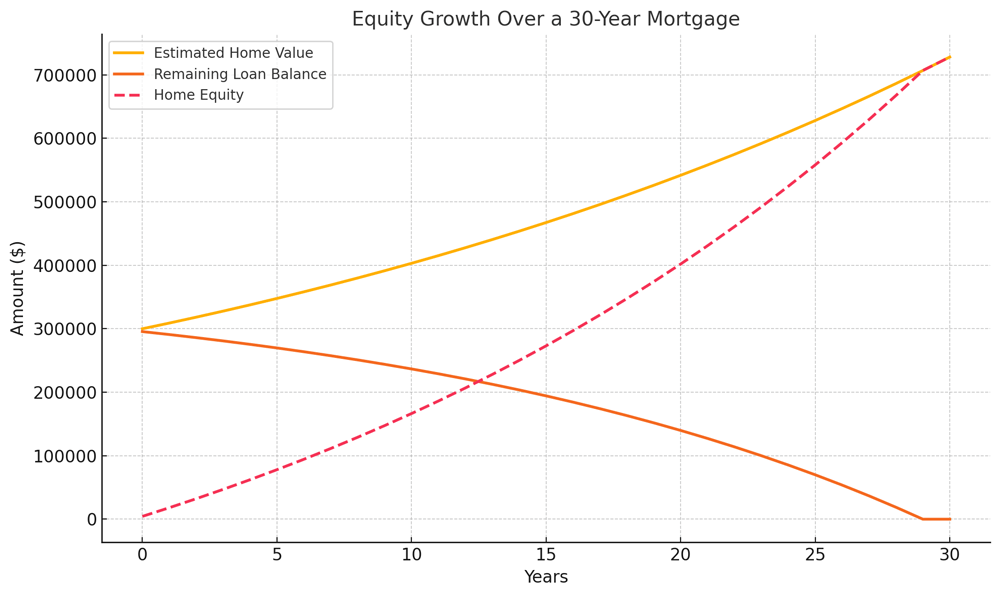

Equity Growth Over Time: A Visual Snapshot

The chart below illustrates a typical equity growth trajectory over the life of a 30-year fixed mortgage with 3% home appreciation and a 5% interest rate. Notice how home equity accelerates in later years as both appreciation and principal reduction compound.

Why the ‘Equity Effect’ Should Reshape Your Financial Mindset

Equity Is a Wealth Multiplier

According to the Federal Reserve (2023), the median net worth of U.S. homeowners is nearly 40 times higher than that of renters—$396,200 vs. $10,400. This disparity is largely due to home equity.

Equity Provides Financial Flexibility

Equity can be tapped for major life events or financial needs through products like:

- Home Equity Lines of Credit (HELOCs)

- Cash-out refinancing

- Reverse mortgages (for qualifying older homeowners)

It’s a versatile asset that can be used to fund college, start a business, or cover emergency expenses—often at much lower interest rates than personal loans or credit cards.

Equity Can Enhance Retirement Planning

Many homeowners plan to downsize in retirement, using the equity from their current home to purchase a smaller one while pocketing the difference. Others may tap equity to reduce living expenses or eliminate debts. Either way, your mortgage payments today become strategic options tomorrow.

Strategies to Build Equity Faster

If you’re looking to accelerate your equity growth, consider these proven tactics:

Make Extra Principal Payments

Even one additional payment per year can reduce your loan term and interest significantly. For example, paying just $100 extra each month on a $300,000 mortgage at 5% can cut your loan term by 4–5 years.

Refinance to a Shorter-Term Loan

A 15-year mortgage builds equity faster than a 30-year option due to higher principal contributions early on.

Increase Property Value with Improvements

Upgrades that improve your home’s value—especially in kitchens, bathrooms, and energy efficiency—can boost equity through appreciation.

The Power of Ownership, One Payment at a Time

The “Equity Effect” is the quiet engine behind the long-term power of homeownership. Every payment made, every dollar invested into your property, and every year of appreciation is another step toward building real, tangible wealth.

At SFMC Home Lending, we’re committed to helping you make the most of your mortgage—not just by closing loans, but by opening doors to lifelong financial opportunity.

If you’re ready to explore how your mortgage can work harder for you, reach out to one of our home lending experts today.

References

- Board of Governors of the Federal Reserve System. (2023). Survey of Consumer Finances. https://www.federalreserve.gov/econres/scfindex.htm

- Federal Housing Finance Agency. (2024). U.S. House Price Index Report. https://www.fhfa.gov/DataTools/Downloads/Pages/House-Price-Index-Datasets.aspx

- Goodman, L., & Mayer, C. (2018). Homeownership and the American Dream. Urban Institute. https://www.urban.org/research/publication/homeownership-and-american-dream

- National Association of Realtors. (2023). Home Price Trends Report. https://www.nar.realtor/research-and-statistics