At SFMC Home Lending, we believe in empowering individuals and families to make informed, confident decisions about their financial future. One of the most critical financial choices many Americans face is whether to rent or buy. While homeownership isn’t right for everyone, the data paints a compelling picture of its long-term benefits—especially when it comes to building wealth, increasing financial stability, and improving credit health.

The Wealth Gap Between Homeowners and Renters

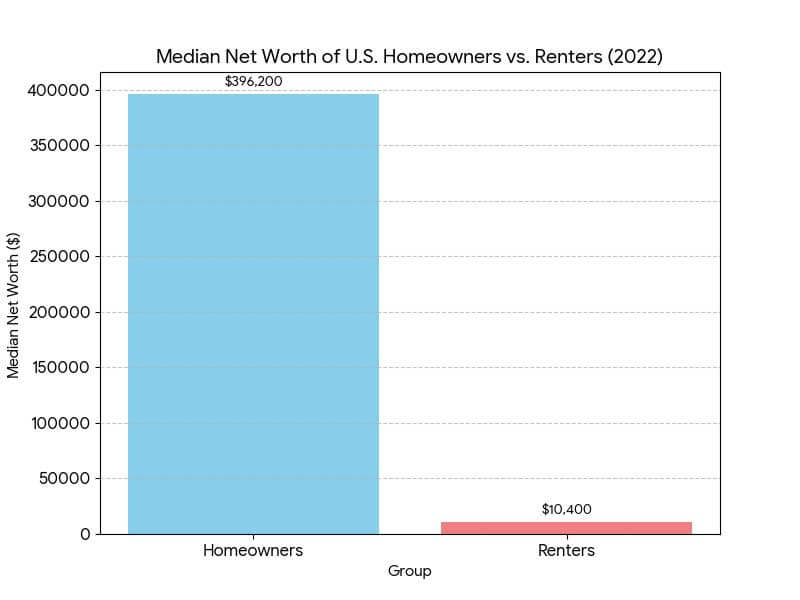

According to the Federal Reserve’s 2022 Survey of Consumer Finances, the median net worth of U.S. homeowners is $396,200, compared to just $10,400 for renters—a nearly 40x difference.

“Homeownership is often the largest single contributor to household wealth,” notes Laurie Goodman, fellow at the Urban Institute.

- Real estate appreciation adds value over time, creating equity.

- Homeowners are more likely to invest in home improvements that increase property value.

- Unlike rent, mortgage payments contribute to an asset that builds long-term value.

Financial Stability and Emergency Preparedness

Research from the Urban Institute finds that homeowners are far more likely than renters to have emergency savings. In fact, 38% of homeowners report having at least three months of living expenses saved, compared to only 20% of renters.

Why this matters:

- Financial cushions reduce stress and improve decision-making during economic uncertainty.

- Mortgage stability often leads to better budgeting habits and long-term planning.

Credit Health and Long-Term Financial Behavior

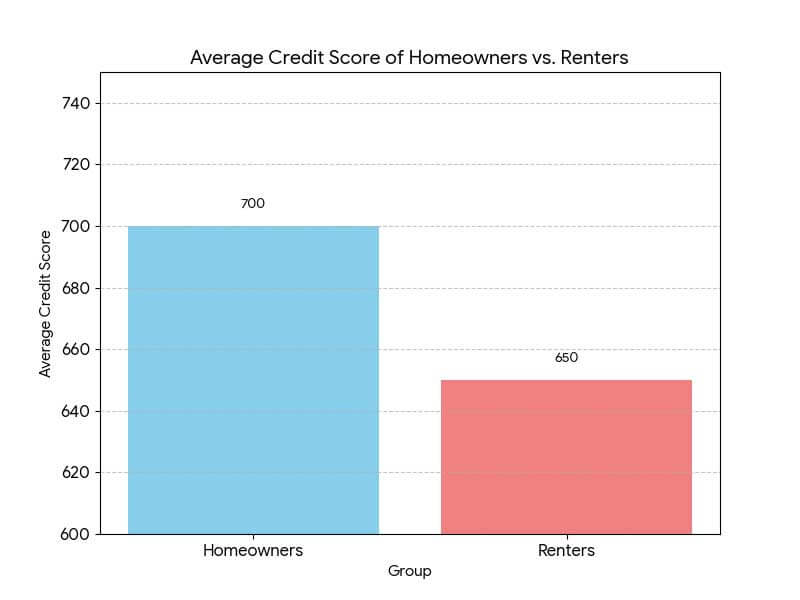

Credit scores are another area where homeowners consistently outperform. A study by Fannie Mae found that the average credit score for homeowners is over 700, compared to approximately 650 for renters.

Improved credit health is often a result of:

- Regular, on-time mortgage payments that strengthen credit history.

- Decreased reliance on high-interest credit due to equity-building behavior.

- Access to refinance or equity loans at better rates due to strong credit profiles.

Educational and Generational Impact

Homeownership doesn’t just benefit the current generation. According to the National Association of Realtors (NAR), children of homeowners are more likely to graduate from college and less likely to experience behavioral problems or economic hardship.

Benefits extend generationally:

- Home equity can be passed down or used to support college education.

- Stable housing leads to better educational and health outcomes.

A Tool for Closing the Racial Wealth Gap

The Urban Institute also highlights homeownership as a key lever in closing the racial wealth gap. While disparities remain in homeownership rates, expanding access to sustainable mortgage options helps narrow the divide over time.

SFMC Home Lending is committed to supporting this progress by offering inclusive lending solutions and educational tools for all communities.

Investing in More Than a Home

When you purchase a home, you’re not just buying property—you’re investing in your future. The numbers are clear: homeowners benefit from greater wealth accumulation, increased financial security, improved credit, and long-term generational advantages.

If you’re considering homeownership, SFMC Home Lending is here to guide you every step of the way—with expert advice, flexible options, and a commitment to helping you succeed.

Citations and References

- Federal Reserve. Board of Governors of the Federal Reserve System. (2023). Survey of Consumer Finances 2022. https://www.federalreserve.gov/publications/files/scf22.pdf

- Urban Institute. Goodman, L., Bai, B., Zhu, J., & Kaul, K. (2017). Homeownership and wealth building: Examining the association between home equity and financial security. Urban Institute. https://www.urban.org/sites/default/files/publication/102016/how-homeownership-contributes-to-wealth-building-and-financial-security_1.pdf

- Urban Institute. (2020). Homeownership and wealth building: A pathway to closing the racial wealth gap. https://www.urban.org/urban-wire/homeownership-and-wealth-building-pathway-closing-racial-wealth-gap

- Fannie Mae. (2016). Housing Insights: Comparing Credit Profiles of Renters and Owners. https://www.fanniemae.com/media/18156/display

- National Association of Realtors. (2023). Social Benefits of Homeownership and Stable Housing. https://www.nar.realtor/research-and-statistics/research-reports/social-benefits-of-homeownership-and-stable-housing